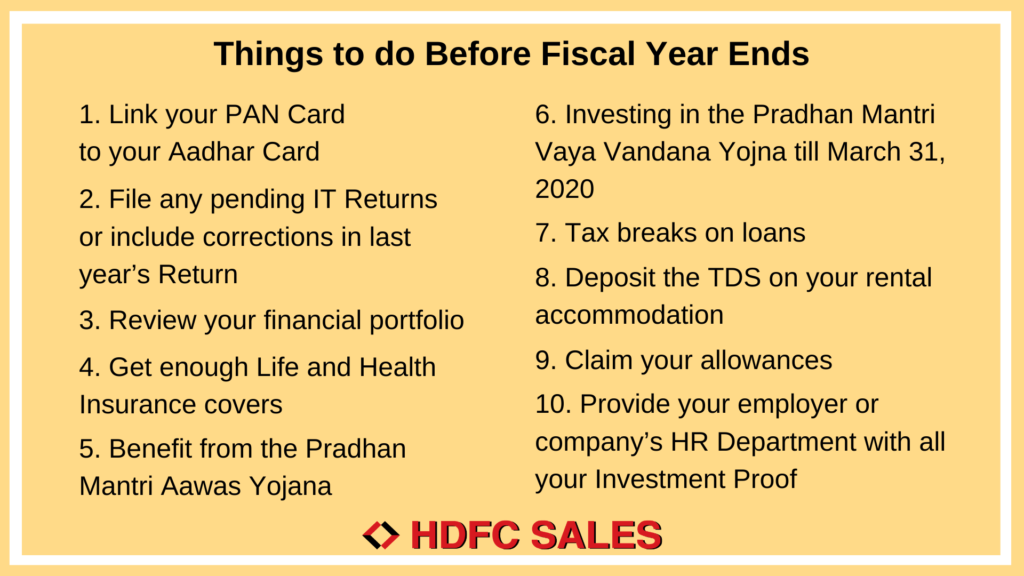

March is the time to see how successful we were in achieving your yearly monetary goals. Fiscal year endings can get stressful if you don’t plan well. So, here are the top ten things for individuals to do before the Fiscal Year 2020-21 ends:

1. If you haven’t, link your PAN Card to your Aadhar Card

Link your PAN Card to your Aadhar Card before March 31, 2021. After the said date, you might not be able to use your PAN Card. It could become invalid.

2. File any pending IT Returns or include corrections in last year’s Return

If you happened to miss filing your Income Tax Returns for the previous year (2019-20), you could still do so till March 31, 2021. The assessing offices might levy a fine of INR 5,000 to INR 10,000 on you but not without giving you a chance to explain the reason for the delay.

If you notice any errors in your previous year’s IT Returns, you can re-submit the corrected one till March 31, 2021.

When you file your returns past the due date, you can’t make any more revisions.

3. Review your financial portfolio

March is an excellent time to conduct your portfolio review. Before you invest for tax-saving, see to what your current Debt to Equity Ratio is. Let’s say, while calculating your risk appetite, you determined that your debt to equity investment ratio is 60:40. Because of a surge in the market, assume your current Debt to Equity Ratio has turned to 30:70. That means you must increase your investments in debt to re-balance your portfolio. So, use Tax-Saving Fixed Deposits to re-balance your portfolio and save tax. In a reverse case scenario, invest in Tax-Saving Mutual Funds.

Before you invest in Tax-Saving Mutual Funds, examine which tax-saving funds have performed well. Do not buy a new Tax-Saving Mutual Fund every year. Top-up the better-performing Mutual Funds this year. Besides saving tax, you will also save up on other costs associated with buying a new Mutual Fund.

As per Section 80C, you can invest up to INR 1,50,000 per year to save tax.

4. Get enough Life and Health Insurance covers

You can also avail tax-breaks on your Life and Health Insurance Plans. Within a year, your circumstances must have changed. When you review your portfolio, see if you need to top-up your existing Life and Health Insurance Plans.

Tax-breaks are also available on health riders in Life Insurance Policies. These riders could be critical illness or health covers.

5. Tax breaks on loans

If you have a Home Loan or a Student Loan, you can avail tax breaks on them.

Home Loans have tax benefits on both the interest under Section 24 and the principal amount under Section 80C. There’s an extra incentive on INR 50,000 given to select first-time home buyers.

For Student Loans, tax benefits are available for a maximum of eight years on the interest amount under Section 80E.

Collect the necessary receipts of EMI payments you have made throughout the year.

6. Investing in the Pradhan Mantri Vaya Vandana Yojna till March 31, 2021

The Pradhan Mantri Vaya Vandana Yojna is a Pension Plan for senior citizens aged 60 years and above. The scheme offers assured returns ranging from 8- 8.3%. The Life Insurance Corporation of India has the exclusive rights to distribute the product.

INR 15 Lakhs is the maximum investment amount per senior citizen. At present, the opportunity to invest in the scheme is available till March 31, 2021.

7. Benefit from the Pradhan Mantri Aawas Yojana

The Pradhan Mantri Aawas Yojana is a unique scheme aimed at providing affordable housing for low and middle-income groups in India. Based on your income group, you can get subsidies on the Home Loan interest rate under the scheme.

If you belong to the middle-income income group and wish to get a credit subsidy under the PMAY, do so before March 31, 2021.

8. Deposit the TDS on your rental accommodation

If you live on rent and your monthly rent exceeds INR 50,000, you have to deposit 5% TDS (Tax Deduction at Source) on your total rent amount. This tax amount will get deducted once a year; when you vacate the premises or if the financial year ends.

If you do not deposit the TDS within 30 days before March 31, you might have to pay the penalty that applies.

9. Claim your allowances

Claim all your allowances if you have incurred any expenses. Submit the necessary bills and related proof to your employer. Claiming your benefits can also help reduce some of your tax liability.

Some examples are HRA- House Rent Allowance, LTA- Leave Travel Allowance, telephone, travel and medical allowances.

10. Provide your employer or company’s HR Department with all your Investment Proof

Once you put everything together, update your company’s HR Department with the information. i.e. Proofs of Investment and loan EMI payments.

For people who have changed jobs midway, give your current employer your previous Employment Payslips.

Disclaimer: HDFC Sales Private Limited, Registered office: 4th Floor, Wing-A, HDFC House, 165-166, Backbay Reclamation, H.T. Parekh Marg, Churchgate, Mumbai – 400020. CIN: U65920MH2004PTC144182; Email: customercare@hdfcsales.com; Toll Free: 1800 266 3345; website: www.hdfcsales.com; IRDAI Reg. No. CA0080.