Today, it doesn’t matter whether you are a homemaker or a working professional. Financial knowledge has become crucial for every woman.

If your finances are in order, you are in a better position to care for your loved ones and pursue your dreams. Financial independence is not a choice anymore. It’s a basic necessity for all.

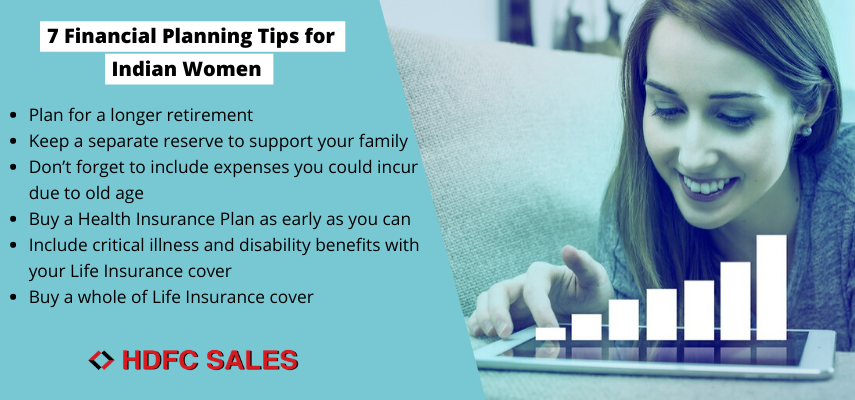

Here are the top seven financial planning tips for Indian women to consider:

1. Plan for a longer retirement

The harsh truth about retirement is that most people run out of money too early. Research has proved that women live longer than men.

Women also have a shorter work life than their male counterparts. In India, the percentage of women who leave their careers to care for their families is one of the highest. Some also take up jobs with a lesser pay to support their families.

Women have to build a larger retirement corpus with limited resources and time.

So, create a rock-solid financial plan. Saving would not be enough. Start early and invest more. Choose Equity Investments. Depending on the amount of time you can devote to your investments, do not have more than 75% of your principal in Equity Investments.

When you withdraw your employer’s Provident Fund, invest it. Don’t spend it.

If you are married, keep a separate investment to generate income for the surviving spouse.

2. Some ways to find the money to invest

- Observe what you spend on. Every time you buy things, ask yourself if it is necessary for survival. With this method, you will be able to distinguish between your needs and wants. Once you build the habit of buying what you need, you will be able to free up quite some money to invest.

- Make a note of your credit card bills and loan EMIs. See which credit card charges you the highest interest. Credit cards have higher interest rates than personal loans. Check if you can take one personal loan and clear all your credit card debt. You can use this method to organize your loans too.

- Give your bank instructions to debit your account when you swipe your credit card. This way, you will only spend what you have.

- We say jewels are our support for a rainy day. Though in reality, they hold emotional value in our life. We tend to avoid selling them. If you love buying gold, use paper assets in place of jewellery. You will save on the making charges. Paper assets will be easier to sell too.

3. Keep a separate reserve to support your family

When the family needs financial help, a woman contributes all she can from her side. Even if that means using her retirement funds.

If you use your long-term investments, thinking you’ll start over soon, you will have to invest a higher amount later. You will lose all the benefits of compounding if you withdraw early.

Keep a separate sum aside instead of digging into your retirement investments. Don’t disturb your long-term investments for emergencies.

4. Don’t forget to include expenses you could incur due to old age

Women perform many duties in the household. When you grow old, health might not permit you to do so. You will have to hire help to do the housework. You might also need an extra full-time attendant or a nurse to take care of you or your spouse.

Hiring an attendant takes quite an amount out of your retirement expenses. When you plan your retirement, don’t forget to create a provision for these costs.

5. Buy a Health Insurance Plan as early as you can

Whether your company gives you medical coverage or not, buy a Health Insurance Policy. It is difficult to predict how healthy you will be when you retire.

If you have a Health Insurance Policy, the insurance company is bound to cover you in old age.

When you go to buy a new Health Insurance Policy at the age of 65, you have to undergo medical tests. You could have to pay a higher premium for coverage. Some companies might refuse to cover you; some might also add extra loading or put a cap to certain benefits for seniors.

6. Include critical illness and disability benefits with your Life Insurance cover

Health Insurance pays only your medical bills. You will incur many other expenses if you suffer from critical illness or disability.

A critical illness cover pays out a lump sum cash if you get diagnosed with any of the listed diseases. The insurance company doesn’t ask you how you spent your critical illness payout. If possible, buy your critical illness cover for the whole of life.

Likewise, a disability cover will help you with the finances to survive in case of disability.

7. Buy a whole of Life Insurance cover

A whole of Life cover can help you provide for a surviving spouse. Choose the option “Joint Life First Death” in the whole of a Life Insurance Policy. With this option, the surviving spouse gets the insurance payout.

With the money they get, they can sustain the later years of their lives.

Warren Buffet has said, “Buy your investments like how you buy your groceries and not like you buy your perfume.”

Patience and control over emotions will make you a better investor.

Always buy quality investments for a bargain price.

Disclaimer: HDFC Sales Private Limited, Registered office: 4th Floor, Wing-A, HDFC House, 165-166, Backbay Reclamation, H.T. Parekh Marg, Churchgate, Mumbai – 400020. CIN: U65920MH2004PTC144182; Email: customercare@hdfcsales.com; Toll Free: 1800 266 3345; website: www.hdfcsales.com; IRDAI Reg. No. CA0080.