Once you have made the decision to buy a house you can call home, you realise it's only the beginning in a long line of decisions that keep getting tougher as you go on. A house will have an effect on your life and financials for decades to come, and loans are curated in many ways to provide the perfect balance of flexibility, risk and stability for the same. Perhaps, HDFC Home Loan is the answer to your dream home. However, the decision around the type of interest rates on your Home Loan is a bit confusing that can be sorted out by weighing the pros and the cons of both.

What are Fixed and Floating Loan Interest Rates?

Before diving deep into comparisons, let’s see what each term actually means.

Fixed Interest Rate:

This type allows the buyer to repay the fixed amount of the loan as equal monthly installments within the given tenure. It’s usually the customers’ first preference as they take this opportunity to lock the interest rate as per their own preference. Most people find it to be the best option available as the interest rate remains the exact same irrespective of the market rate fluctuation.

Floating Interest Rate:

This type is very volatile and the interest rate fluctuates as and when the base rate offered by various lenders change. Though it’s comparatively cheaper than Fixed Interest Rates by 1%-2.5%, it might turn out to be difficult to plan the budget especially when the market rate goes up and the interest increases.

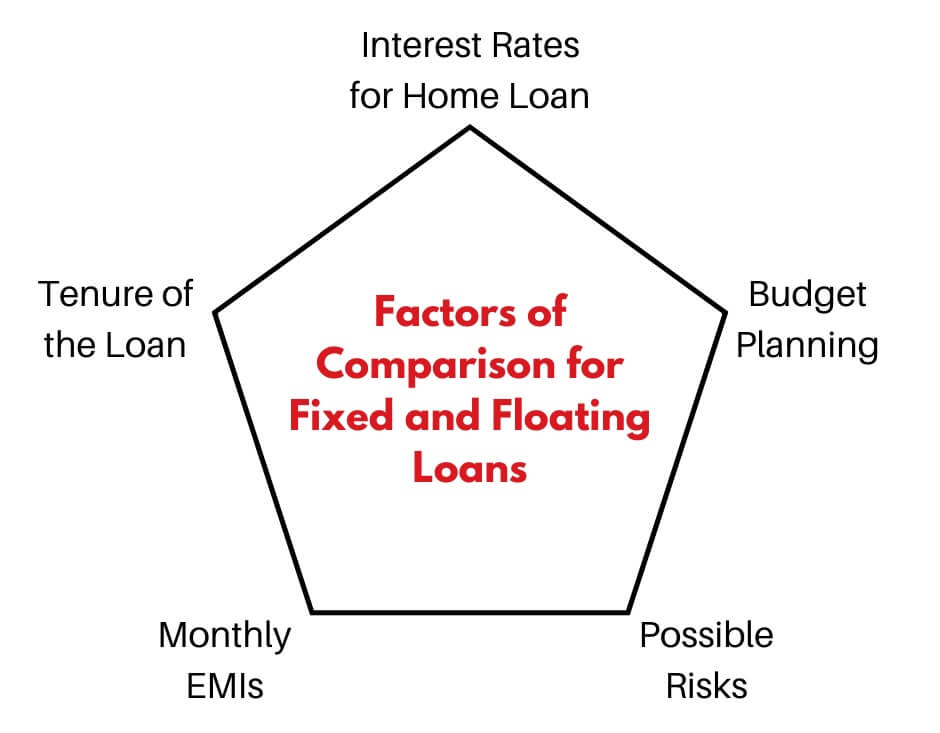

Comparing Fixed Loan and Floating Loan Interest Rates

1.Interest Rates for Home Loan:

Floating Interest Rates are usually lower than Fixed Interest Rates but can go high up or low down as per the market trend.

2. Monthly EMIs:

In case of Fixed Interest Rates, the monthly EMIs remain the same while that of Floating Interest Rates increase or decrease according to the market rates.

3. Budget Planning:

If you’re on a budget plan, Fixed Interest Rates are a better option than Floating Interest Rates as the latter is affected by the rise in the market rate unlike the former.

4. Tenure of the Loan:

While people over 40 years prefer Fixed Interest Rates (10 years’ tenure), ones in their mid-20s choose Floating Interest Rates due to a longer duration of repaying the amount at cheaper rates (20-30 years).

5. Possible Risks:

If you’re looking for certainty, even during volatile conditions, Fixed Interest Rates are the best option for you. However, if you can pay only a little bit higher during high rate durations, Floating Interest Rates can be cheaper in the long run, especially when the market goes down.

Conclusion

It’s best to choose the loan type that fits your income and other needs the most. Thus, before choosing, research well about all the HDFC Home Loan Plans and put forward your best foot to suit your requirements in the future.

Disclaimer: All loans at the sole discretion of the HDFC Ltd. For detailed Terms and Conditions, visit www.hdfcsales.com; Toll Free: 1800 266 3345.