The Indian Government has always tried to encourage citizens to buy homes. This is why the Home Loans qualify for the Section 80C tax deduction. In addition, when you buy a house with a Home Loan, you get a slew of tax perks that help you save money on your taxes.

For the current Fiscal Year 2021-22, an individual can use the old tax system and claim special tax breaks such as HRA and different reductions under Sections 80C, 80D, and so on. Individuals have an option of participating in the new regulatory framework (which has lower tax burden and no tax exemptions) or adhering to the old regulatory framework.

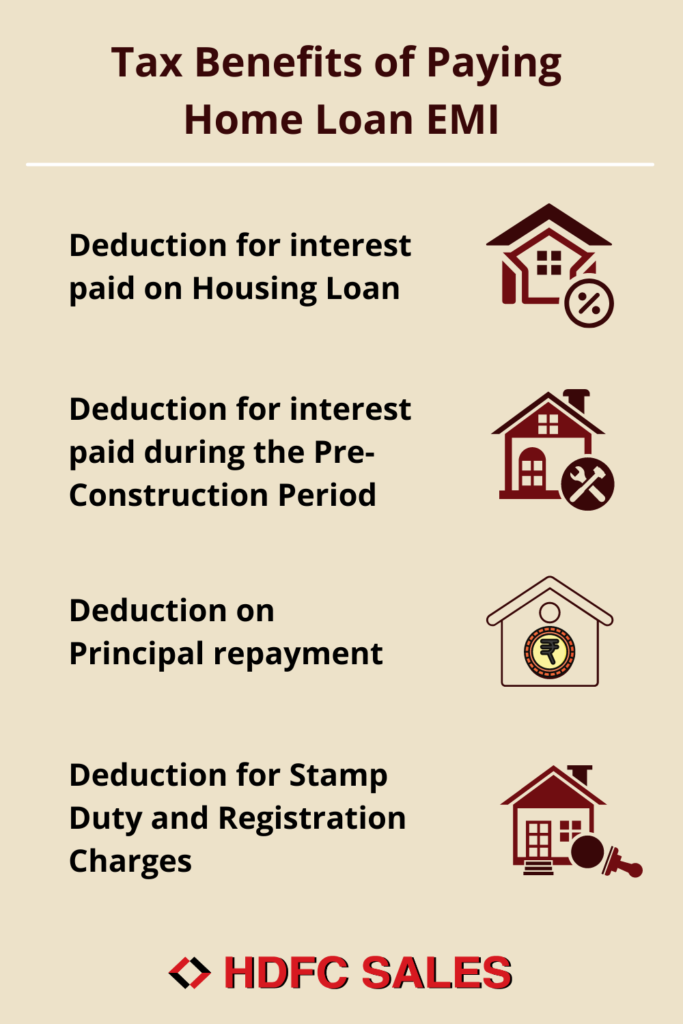

Tax benefits of paying Home Loan EMI

Deduction for interest paid on Housing Loan

The home constructed or acquired by the policyholder must be finished within 5 years of the financial year in which the loan was obtained. HDFC Home Loan interest rate starts from 6.75% per year and offers extra features such as flexible repayment choices and a Top-Up Loan.

Section 24 lessens the burden of a part of your EMI paid for the year from your total income. It can go up to ₹2 Lakhs. This exemption is available beginning with the year in which property is constructed.

Deduction of interest paid during the pre-construction period

Over and above the deductions you are otherwise able to claim from your house property income, the income tax law provides you the facility to claim such interest, known as pre-construction interest. However, the highest amount that may be claimed is ₹2 Lakhs.

Deduction on Principal repayment

Under Section 80C, the principal share of your EMI during the year is deducted. The limit of the claimed amount is up to ₹1.5 Lakhs. However, the residential property must not be sold during 5 years of occupancy in order to claim this credit. Otherwise, the earlier reduction will be deducted from your income in the year of sale.

Deduction for Stamp Duty and Registration Charges

Apart from the deduction for financing amount, the fee for Stamp Duty and registration can also be taken off, under section 80C. This claim can be made in the year in which the expenditures are made, though.

So, assuming you match the required circumstances, all House Loan-related deductions combined can enable you to receive a maximum deduction of ₹5 Lakhs (₹2 Lakhs u/s 24, ₹1.5 Lakhs u/s 80C, and ₹1.5 Lakhs u/s 80 EEA). If you want to own a new home, you can structure your purchase so that your loan helps you earn the most of tax deductions.

Disclaimer: All loans at the sole discretion of the HDFC Ltd. For detailed Terms and Conditions, visit www.hdfcsales.com; Toll Free: 1800 266 3345.